CRA Partnership Frequently Asked Questions (FAQs)

The Opportunity

A 1977 federal law called the Community Reinvestment Act (CRA) encourages banks to make investments to benefit low- and moderate-income individuals and neighborhoods, including workforce development-related activities for people with disabilities.[i] CRA activities can take many forms, from the development of financial services career pathways to financial education conducted by bank employees.

This frequently asked questions (FAQ) was developed for workforce development boards and their staff members, community colleges, and others who provide workforce services. The FAQ provides answers to questions about workforce system–bank partnerships listed below.

FAQs

- What is the Community Reinvestment Act?

- What kinds of activities can banks engage in with workforce systems to support their CRA requirements and increase career success for individuals?

- Why focus on people with disabilities?

- What are some examples of partnerships between the workforce system and banks?

- What financial education benefits are possible under the Workforce Innovation and Opportunity Act?

- What additional resources can facilitate understanding of and access to the benefits of the Community Reinvestment Act?

What is the Community Reinvestment Act?

The CRA is a 1977 law that sought to leverage the financial resources of private sector institutions to assist with community development. Banks receive CRA credit for participating in and funding activities in low- and moderate-income neighborhoods in their communities. The CRA defines a low-income community as a community with a median family income that is less than 50% of the area’s median income.[ii] A moderate-income community has a median family income that is at least 50% but less than 80% of the area’s median income.[iii]

To receive CRA credit for community development, a bank must have at least one of the following as its primary purpose:

- Community services targeted to individuals who have a low- to moderate-income;

- Activities that promote economic development, such as job training or financial education;

- Activities that revitalize or stabilize low- and moderate-income communities; or

- Initiatives that create or sustain affordable housing.

The CRA’s requirements apply to all banks, depending on the size of the institution. Credit unions do not have any requirements under the CRA, but they can be partners in financial education work.

What kinds of activities can banks engage in with workforce systems to support their CRA requirements and increase career success for individuals?

Banks can engage in a variety of activities with workforce systems to increase career success and financial security for people with disabilities, while supporting and meeting CRA requirements. [iv] Among many other opportunities, these include:

- Teaching financial education, delivering the Federal Deposit Insurance Corporation (FDIC) Money Smart program, or offering financial counseling in workforce development programs;

- Providing donations to workforce development programs designed to improve employment opportunities for low- to moderate-income individuals with disabilities;

- Providing financial capability training to individuals with disabilities;

- Providing volunteer service with nonprofits to provide income tax assistance for low- to moderate-income individuals;

- Serving on workforce boards; or

- Helping to establish pipelines of talent to meet the needs of the financial services sector through apprenticeship or other work-based learning.

Why focus on people with disabilities?

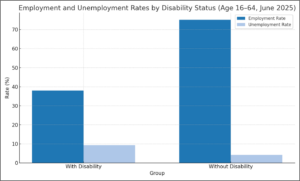

Indicators such as national employment rates, unemployment rates, and the banking/lending practices of people with disabilities signal challenges that hinder achievement of economic self-sufficiency. Exhibit 1 shows that In June 2025, 38 percent of individuals with disabilities were employed compared to 75.1 percent of individuals without disabilities, and the unemployment rate for individuals with disabilities was 9.3 percent compared to 4.2 percent for individuals without disabilities.

Exhibit 1: Employment Data [v]

According to a 2023 report from the Federal Reserve Bank, significant disparities in access to financial services persist, particularly among individuals with low incomes and those with disabilities. In 2023, 23 percent of adults earning less than $25,000 annually were unbanked, compared to just 1 percent of those with incomes of $100,000 or more. Similarly, 11 percent of individuals with a disability were unbanked, more than double the rate of 5 percent among those without a disability.[vi]

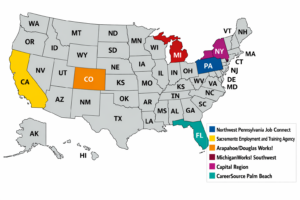

What are some examples of partnerships between the workforce system and banks?

Below are descriptions of six workforce–bank partnerships in Pennsylvania, Florida, California, Colorado, Michigan, and New York.

Banking Roundtable and Northwest Pennsylvania Job Connect (Erie, Pennsylvania)

Northwest Pennsylvania Job Connect used Banking Roundtables to strengthen relationships between the workforce system, community development organizations, vocational rehabilitation, and local financial institutions. Through these discussions, partners explored workforce needs within the banking sector, including occupations experiencing staffing shortages and the skills needed for those positions. The roundtables also created opportunities to discuss career pathways in financial services and how workforce and disability-serving partners could better connect job seekers, including Americans with disabilities, to careers in the sector.

As a result of these efforts, local banks increased job postings on Pennsylvania’s workforce development system website, representing a variety of occupations and locations. Job Connect and its partners also collaborated with financial institutions to offer budgeting, financial literacy, coaching, and mentoring opportunities for job seekers. In addition, Job Connect referred customers to a newly established financial literacy center at a partner bank, helping expand access to ongoing financial education while strengthening collaboration between workforce and banking partners.

Building Bank Partnerships and CareerSource Palm Beach (West Palm Beach, Florida)

CareerSource Palm Beach strengthened connections between the workforce system, financial institutions, and community partners while expanding access to financial education and career opportunities in the financial services sector. CareerSource Palm Beach hosted a “Building Financial Wellness” event that brought together workforce, banking, and community development partners to discuss strategies for supporting job seekers and businesses through financial wellness and training initiatives. This effort also led to collaboration with the Federal Deposit Insurance Corporation (FDIC) to incorporate the FDIC Money Smart curriculum into American Job Center service delivery.

CareerSource Palm Beach also reviewed learning paths and training programs offered by education partners to better understand local financial services workforce needs. In addition, the site developed a feedback process to gather information from banking partners on hiring needs and workforce priorities. Through meet-and-greet sessions and ongoing collaboration with workforce boards, vocational rehabilitation staff, and community development partners, the pilot strengthened relationships across systems and helped align workforce training efforts with careers in the financial services sector.

California Capital Financial Development Corporation and Sacramento Employment and Training Agency (Sacramento, California)

The Sacramento Employment and Training Agency (SETA) developed a partnership with the California Capital Financial Development Corporation. As a result of this partnership, job seekers can access the following financial capability services through the workforce system:

- financial education;

- financial resources;

- financial counseling;

- financial assistance for entrepreneurs; and

- a Financial Empowerment Center (FEC).

In addition, the City of Sacramento established a FEC through the Bank On model. Bank On provides unbanked and underbanked individuals and families with asset building, banking access, consumer financial protection, and financial education and counseling. Financial Empowerment Centers (FECs) offer professional, one-on-one financial counseling for local residents. Trained counselors help individuals pay down debt, increase savings, establish and build credit, access safe and affordable banking products, and build assets for long-term financial health. The city has integrated the FEC work with its overall strategy for building economic opportunities. Using prior funding, the International Rescue Committee, a local community-based organization, provided training through the FEC, and one of the team members from the workforce system became certified as an FEC instructor/coach.

Multiple Banks and Arapahoe/Douglas Works! (Denver, Colorado area)

The workforce system in Arapahoe and Douglas Counties, Colorado, partnered with Goodwill Industries of Denver in their BankWork$® program. BankWork$® provides young adults with training for entry-level positions in banking as well as work experience, coaching, and placement into careers in the financial industry. Wells Fargo and Bank of America support this workforce development approach nationally, and the Colorado Bankers Association endorses it. The following local partner banks also participate: Academy Bank, Bank of America, Bank of Denver, Bank of the West, Citywide Banks, KeyBank, U.S. Bank, Vectra Bank, and Young Americans Bank.

The BankWork$® model is a service and investment partnership between banks and the workforce system.

Multiple Banks and MichiganWorks! Southwest (Kalamazoo, Michigan)

Youth Opportunities Unlimited (YOU) — a division of Kalamazoo Regional Educational Service Agency (KRESA), the Workforce Innovation and Opportunity Act (WIOA) youth provider for MichiganWorks! Southwest — has developed partnerships with banks through KRESA’s new Career Awareness and Exploration team. This team established the Financial Literacy FinLit Fanatics Committee, consisting of a variety of banks, credit unions, and career coaches focused on providing financial education experiences to K-12 students.

The FinLit program uses a two-generation approach to support financial stability. This program pairs youth participants with a known adult (e.g., parent, mentor, guardian) and together they participate in workshops on job seeking, financial empowerment, and educational opportunities.

Multiple Banks and Albany-Rensselaer-Schenectady County–Capital Region (Albany, New York)

Since 2001, the Creating Assets, Savings, and Hope (CA$H) Coalition has brought together banks and community-based agencies, including the workforce development board in Albany, New York, to provide programs that increase the financial capabilities of people with disabilities and others in the low- and moderate-income population. The Cities for Financial Empowerment Coalition spearheaded the development of the CA$H Coalition; Wildwood, an area nonprofit agency that is a part of the workforce system, leads the program.

Known more widely as Bank On, the effort engages job seekers, especially people with disabilities, in the following activities and programs:

- financial capability workshops, where volunteers from banks and credit unions join other professionals to provide training;

- FECs, where staff from financial institutions volunteer and donate resources and expertise, including strategies for accessing bank and credit union services;

- financial-wellness coaching, where financial institutions offer one-on-one coaching in their own facilities upon referral; and

- volunteer income tax preparation, where volunteers from the community, including bank employees, with some funding support from the IRS, help people complete their tax returns.

Bank and workforce partners are developing financial industry career paths and will ensure that qualified job seekers with disabilities will be aware of, and available to, enter this pipeline.

What financial education benefits are possible under the Workforce Innovation and Opportunity Act?

WIOA supports the provision of financial education activities for adults and youth and includes specific language intended to improve outcomes for individuals with disabilities and individuals with multiple challenges to employment.[vii] These provisions promote financial empowerment, enabling job seekers to increase their economic self-sufficiency and to participate in their communities. Promising career pathways programs also incorporate financial capability training to help people with disabilities successfully manage their finances once they obtain employment.

In WIOA Title I Adult Programs, adult job seekers can participate in financial education activities as appropriate, to meet their employment goals and objectives. The assistance can include skills development to attain career objectives, individual and group counseling, short-term prevocational services, communication and interviewing skills, internships and work experience, as well as financial education services.

The WIOA Title I Youth Program includes financial literacy education as one of 14 services that must be available to youth participants. WIOA youth financial education provides individuals with the skills and knowledge they need to achieve long-term financial stability. As listed in section 129 of WIOA, these skills and knowledge include making and using budgets, saving, planning effectively for education and retirement, and using credit as well as financial products and services effectively.

Title IV of WIOA—the State Vocational Rehabilitation Services Program—provides funding to help individuals with disabilities prepare for, obtain, and retain employment. These services may include financial literacy training, which supports long-term employment success and economic self-sufficiency. In coordination with other WIOA titles, Title IV helps individuals with disabilities gain the financial skills needed for greater financial stability. For students with disabilities, Pre-Employment Transition Services (Pre-ETS) may also incorporate financial literacy as part of Workplace Readiness Training—one of five required Pre-ETS activities. This training focuses on developing the social and independent living skills essential for success in the workplace and covers key expectations of prospective employers.

What additional resources can facilitate understanding of and access to the benefits of the Community Reinvestment Act?

“Hands On Banking” Quick-Reference Guides and Disability Supplemental Guides

Hands On Banking quick-reference guides provide information and resources that address 15 different barriers that individuals with disabilities may experience. The disability supplemental guides cover disability sensitivity and information to complement the Hands On Banking instructor guides for adults, young adults, and entrepreneurs. Subjects include employment, money management, protected savings, work supports and other financial capability topics relevant to individuals with disabilities. These guides also provide numerous tips, tools, resources and links to Hands On Banking materials.

This report, published by the Federal Reserve Bank of Philadelphia in October 2017, summarizes innovative activities from banks’ CRA performance evaluations in the areas of job creation, education, workforce development, transportation, and affordable housing. The document highlights real-world examples featuring banks who promoted economic growth and prosperity in their communities while receiving credit under the CRA.